ARR Global Long / Short Equity Strategy

ABOUT

ARR Investment Partners

We believe that a disciplined and repeatable process is the cornerstone of successful investing. Our approach is dedicated to delivering strong, consistent, risk-adjusted returns across diverse market cycles and macroeconomic events.

ARR is a London-based investment boutique specialising in advising a global equity long/short quantamental strategy tailored for professional investors. After building a 5+ year SMA track record, ARR has launched a Cayman fund in February 2026.

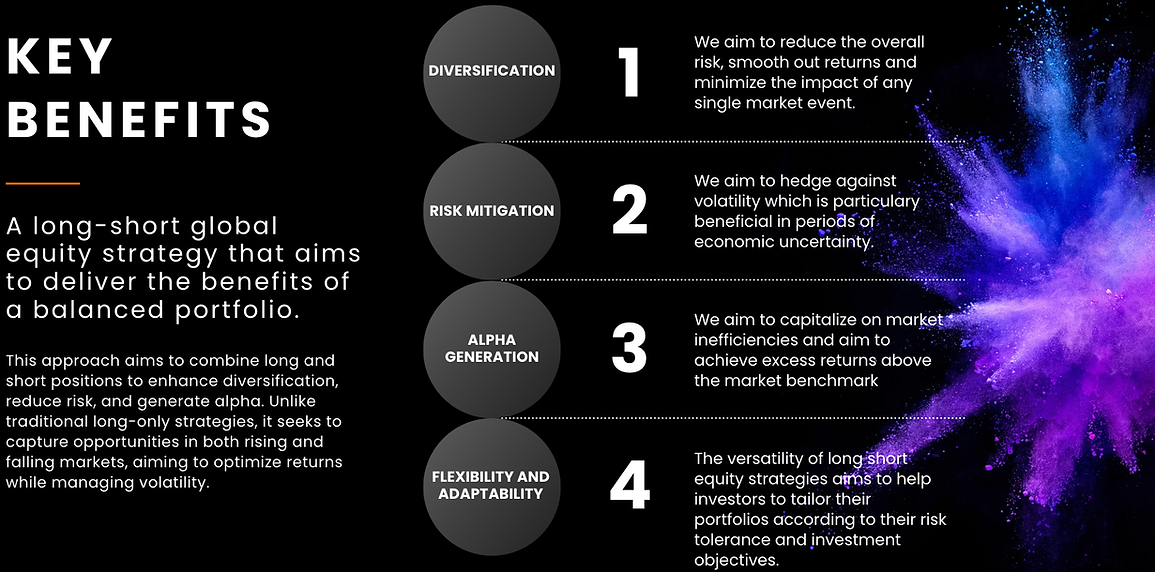

Our primary objective is to generate attractive long-term returns by excelling during market downturns while maintaining robust performance during rallies. This dual focus is achieved by targeting opportunities—both long and short—with what we assess as ‘asymmetric risk-reward’ potential.

Our commitment to excellence has been recognised: ARR proudly won the “With Intelligence HFM European Performance Awards 2024” in the category Global Equity Under $500m. More information can be found here.

INVESTMENT PHILOSOPHY

At ARR Investment Partners, our strategy is designed to generate attractive returns during favorable market trends while maintaining a low or negative correlation to global equity indices during market downturns. By combining a bottom-up approach, which leverages strong single-stock movements, with top-down risk management to navigate broader market corrections, we strive to deliver consistent, risk-adjusted returns.

Avoiding capital loss during severe market corrections is a cornerstone of our philosophy.

To sharpen our competitive edge, we developed PARIS, a proprietary portfolio and risk management system that delivers deep analytical insights.

PARIS operates as a dynamic, evolving loop, encompassing six critical phases: backtesting, idea screening and generation, in-depth analysis, implementation and position sizing, continuous monitoring and risk management, and post-trade analysis—each phase designed to drive continuous improvement and optimisation.

INVESTMENT PROCESS

At ARR Investment Partners, we employ a ‘quantamental’ approach, combining quantitative and fundamental analysis to create a robust and repeatable investment process. Key steps in this process are optimised and, where possible, automated within our proprietary system, PARIS.

From a universe of over 7,000 liquid stocks, PARIS screens and identifies daily investment opportunities that align with our four core patterns: Rebound, Dynamic Profit Growth, Bubble, and Structural Losers. These ideas are further vetted through fundamental analysis to understand their business drivers.

The result is a portfolio of high-conviction long and short positions, with overall risk managed through sector or index ETFs and futures. A strict stop-loss philosophy is integral to our process, ensuring disciplined risk control and protecting against adverse market movements. This disciplined, data-driven approach ensures consistency, transparency, and adaptability across varying market conditions.

OUR TEAM

Highly experienced throughout economic cycles

Christian Putz

Founder, CEO and Portfolio Manager

Christian has led the ARR Global L/S Equity strategy since 2015. Previously, he managed the Long/Short Equity Master Fund at Kazimir Partners, specialising in Eastern European markets. His career began at MAN Group in 2006, an alternative investment firm with AUM >$100 billion, where he worked across asset classes including Credit, Venture Capital, and FoHFs. An active investor since 1997, he holds dual Master’s degrees in Business Administration and International Business & Economics from the University of Innsbruck.

Natalie Pullan

Chief of Staff

Natalie Pullan leverages over a decade of leadership experience in non-profit organisations and associations. As the founder and Managing Director of Events & Administration Management Services (E.A.M.S.), she led her team in managing administration and events for diverse clients, including YPO Chapters. Known for her detail-oriented and adaptable approach, Natalie has implemented effective systems for workflow and project management. She holds a Bachelor of Commerce from The University of Melbourne and has completed several executive education programs at Melbourne Business School and London Business School.

Neil Cowhig

Co-Sourced Chief Operating Officer

Neil is a highly experienced operations professional with over 30 years of expertise in the finance industry. He has worked both as COO/CCO for hedge funds and as an ODD professional for a major hedge fund investor. Before working on the buy side, Neil ran product control for several hedge fund-facing businesses at Deutsche Bank and Nomura, including stock lending and Prime Brokerage businesses. Neil began his career at BDO as an auditor specialising in finance and trained as a Chartered Accountant. Neil holds a Physics degree from Liverpool University.

Yuting Li

Quantitative Financial Analyst

Yuting develops systematic trading strategies, performs quantitative portfolio analysis, and manages risk. Previously, he researched reinforcement learning and portfolio management at Imperial College and worked as a research analyst at JYAH Asset Management, a quant hedge fund in Shanghai. Proficient in C++, Python, R, and SQL, Yuting holds a First-Class Honours degree from Warwick Business School and a distinction from Imperial College London.

Amir Dehkordi

Quantitative Developer

Amir integrates Artificial Intelligence into investment and trading processes, building tools for portfolio managers that enhance decision-making and portfolio analysis. He brings experience as a Quantitative & Generative AI Researcher at a FinTech company and as a Quantitative Analyst at an algorithmic trading firm in London, where he focused on systematic strategies and market microstructure. Amir holds a Distinction in M.Sc. Financial Engineering from the University of Birmingham.

Kevin Ferizolli

Investment Analyst

Kevin supports equity research and investment analysis at ARR Investment Partners. Previously, he interned at a London-based real estate private equity firm, gaining experience in acquisitions and asset management. Skilled in financial analysis and sector research, Kevin holds a BSc in Economic History from the London School of Economics.

Yves Bowonnaowarux

Investor Relations

Yves manages investor communications, reporting, and engagement at ARR Investment Partners. Prior to joining ARR, she advised listed companies and government bodies on strategic communications and public relations. Skilled in stakeholder engagement and investor relations, Yves holds an MA in International Relations from King’s College London and a BA in History from the University of Exeter.

Theron De Ris

Regulation and Compliance

Theron De Ris is the CEO of Eschler Asset Management, providing portfolio management and compliance services to professional investors. Previously, he was a senior research analyst at Indus Capital Partners and held roles at Morgan Stanley in Milan and London, leading the global equity institutional desk. He graduated Magna Cum Laude from Middlebury College in International Politics and Economics.

.png)